Planning for retirement isn’t easy. It’s complex and has many moving parts. For one thing, you will need to have enough income to last for the rest of your life once you step away from a full-time career.

Taxes, healthcare, and inflation are just a few things that can eat into your money. Not only that, you might have a longer retirement than you would think. Nowadays, thanks to advances in healthcare and technology, many people are spending as much as one-third of their lives in their post-retirement years.

How, then, can you plan for a financially confident future? A financial professional’s guidance can help you go the extra mile in many ways. They can help you evaluate your current financial progress. They can also help you spell out your goals, foresee retirement risks, and build personal strategies to assist you in your objectives.

Here are a few ways that hiring a financial advisor or agent can help your retirement in the long run. Read More

With record numbers of baby boomers retiring, many new trends are coming into the retirement landscape. Among boomers, there is one growing trend of “solo agers,” or those who retired without marrying anyone or having any children. According to the American Society on Aging, around 20% of boomers fit this trend.

If you are a solo ager, here are some questions to ask when planning for your retirement. How you answer these questions can be crucial in helping you enjoy a comfortable and financially confident retired lifestyle. Read More

So, you have decided that an annuity makes sense for your retirement. But what type of annuity might be right for you? This will depend on the answers to a variety of questions.

What is your risk tolerance? What timeline do you have for your money? What annuity guarantees are important to you? What you hope to accomplish with the annuity contract? All of these considerations and more are relevant to what annuity might be a good fit for you.

Here are some questions to consider as you think about what annuity might be right for your situation. Read More

Editor’s Note: The following article is a retirement guest post that has been authored and contributed by John Freeman.

Watching our parents age can be difficult as they begin to need more assistance with different aspects of their lives. While your parents likely want to maintain as much of their independence as they can, and they should, you should be there to lend a helping hand when they need it.

More than 65 million Americans provide care for an aging, chronically ill, or disabled family member each year. And, since the U.S. has an aging population, with geriatrics outweighing younger demographics, more and more individuals will be taking on this role—many of whom are not adequately prepared.

If you are one of these individuals, or are simply trying to figure out how you can be useful to your parents as they age, there are certain aspects of their lives that you can help them handle to make the transition easier, starting with these 5 things. Read More

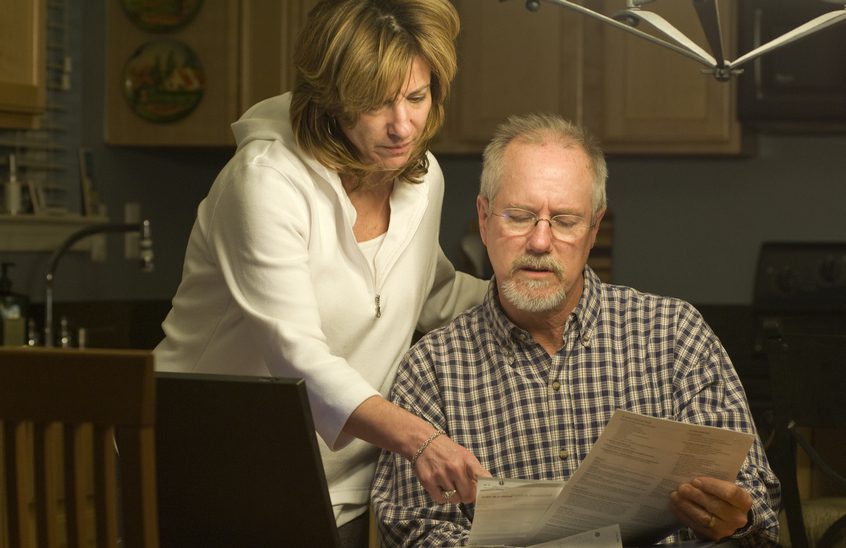

Earlier in your career, you focused on saving and growing your money so you could pursue your financial goals later in life. You might have worked with a financial advisor to do this.

Over the years, you socked away money in a retirement account and maybe even grew an overall portfolio. That meant having and following a strategy with a focus on accumulation and asset allocation. But as we reach the so-called retirement red zone — that crucial period of a decade before and into retirement — new planning is essential.

The income you earned from your career likely won’t be the same once you retire. Then there is the challenge of making your money work for you.

How do you ensure that the income you draw from your portfolio is as efficient and tax-wise as possible? You want to be sure that your money lasts as long as you need it to in retirement! Read More

Franklin Templeton’s annual Retirement Income Strategies and Expectations Survey (RISE Survey) for 2020 has been released. This is the ninth year the RISE Survey has been published, offering valuable insights from Franklin Templeton’s RISE Study.

The survey examines the concerns and attitudes of retirement savers, providing interesting data for both planners and savers. It features insights from various generations on their readiness for retirement and their strategies for achieving financial goals before stopping work.

As usual, this year’s RISE Survey offers valuable insights from Franklin Templeton’s RISE Study. Here’s a roundup of some findings that might be helpful for your own retirement planning efforts.

Read More

Annuities can bring more stability and certainty to a retirement portfolio. But how do you know you are getting a good deal for your money?

The biggest advantage that annuities can give for your retirement is their guarantees. Or in other words, the contractual assurances that the contract-issuing insurance company promises to provide you.

For your retirement, you might already have a number of financial guarantees that will contribute to your retirement security.

You paid into the coffers of Social Security during your career. In exchange, Uncle Sam guarantees you will receive a monthly paycheck from the SSA once you begin your benefits.

If you buy Treasury securities, you are guaranteed a return of your initial principal once the bonds mature. The bonds also pay you guaranteed semiannual interest payments during the maturity period. You also have these same guarantees when you hold a CD from the bank. Read More

In the wake of the coronavirus pandemic, a new study shows that Americans are becoming increasingly anxious about their finances.

Back in April, Fidelity asked 3,062 retired and working-age Americans about their concerns and what they were doing to shore up their confidence gap. In the survey, 60% of Americans said they were concerned about their finances now. Thirty-eight percent were extremely or very concerned, while over twenty percent were just moderately concerned.

Six in 10 (62%) Americans said they worried about job security, with 43% being extremely or very concerned. 51% of baby boomers said they were worried about their finances over the next 6 months. Meanwhile, 69% of millennials and 68% of Gen Xers also shared that concern. Read More

While times change, the need for quality financial guidance doesn’t. Many financial advisors do things old-school. Nevertheless, with everything happening right now, that might well be changing.

It may not be the most exciting topic around, but working with a virtual financial advisor can be beneficial in many ways.

You don’t have to take time out of your busy schedule to go to an office location. Nor do you have to worry about the logistics of what it would take to make that appointment.

You don’t even have to be in the same city as where your financial professional resides. Virtual advisors use communication methods such as videoconferencing, email, the internet, and (for some) even texting to stay in contact with their clients.

If you aren’t working with a virtual financial professional yet, here’s a look at how it can be beneficial in the short and long run. Read More

If you asked a hundred financial advisors about what they use to construct retirement strategies, you would surely get as many opinions as there are flavors of ice cream.

Many portfolio strategies today call for strategic mixes of equities and bonds. Lots of research is on the so-called 60/40 portfolio, made up of 60% equity assets and 40% bond assets.

The problem is that bonds are particularly vulnerable to interest rate risk, which is the danger of an asset losing value when interest rates rise. And with interest rates sitting at basically zero percent for the foreseeable future, the only direction they can go is up.

This isn’t to say that bonds don’t have a place in a retirement income strategy. But there is also the flip-side to consider.

Do you really have all options on the table if your advisor leaves annuities out of the conversation? Unlike bonds of any sort, annuities are unique in that life insurers include estimates of people’s expected mortality into their payouts. Read More