How Much Money Do I Need for Retirement?

Determining how much money you need in retirement is both a mathematical and a personal issue. Like a fingerprint, the answer is unique to you and your spouse.

That is why it’s so important to discuss your 30-year retirement plan early – or in other words, definitely some time before you actually retire. And just not early, but often. This approach will help ensure you and your spouse are on the same page.

Here are a few guidelines you can use in your determination of how much money you need in retirement for a comfortable lifestyle.

How Much Income for Retirement?

Here’s an important question to consider. How much income will you need for a financially secure retirement?

Your 30-year retirement plan will be an invaluable tool in answering this question. Based on an audit of your plan, here are a few financial situations which you might fall under:

1. Level I, below break-even: The total of all income streams in retirement you have accumulated and plan for, may be less than what you want to spend, but your plan is to siphon off assets to plug the gap.

That generally isn’t a good idea and could leave you high and dry over the long term. You should figure out how you might adjust your expenses and/or continue to work and save as long as you can before retiring so that your income/expense model is at least break-even.

2. Level 2, break-even: Expenses are being covered by income, but there is no margin for safety. This is still not where you want to be, so you should work, save, and plan to achieve at least Level 3.

3. Level 3, break-even with a “cushion”: Your projected income will comfortably cover your expenses with an annual surplus. This is a good spot to be in and what all retirees should shoot for.

4. Level 4, break-even + a cushion + a reasonable surplus (potentially estate to pass on to your heirs): This would be great and generous, but if push comes to shove, it is entirely optional.

Modeling the Arc of Retirement in Your Plan

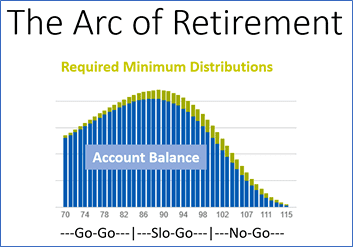

If you were to graph the process of life through retirement, it would look like climbing up a hill on one side to the peak. From there, it would slowly descend on the other side of the hill to the valley below.

We might call this the “Arc of Retirement,” driven by the inevitability of aging and its impact on people’s lifestyle conditions as well as quality-of-life. That includes the rise and fall of someone’s health, energy, strength, and cognitive capacities.

What is interesting to observe (and by design), is the shape of the “decumulation curve” of required minimum distributions (RMDs). This decumulation curve is itself a visualization of the Arc of Retirement.

Required minimum distributions apply to pre-tax accounts such as 401(k)s, 403(b)s, 457s, and traditional IRAs.

The Arch of Retirement and Its Ties to Retirement Finance

The Arc of Retirement can inform one’s forecasts of the rise and fall of income, expenses, and capital and investment expenditures for such items as:

- The intensity and spending for travel, entertainment, sports, food, beverage, and the ability to maintain a house & lawn

- Employability and related income

- The transition from complexity to simplicity

- Financial assistance and/or support for aging parents

- The financial support of kids and grandkids

- The tolerance for risk of portfolio losses

Using a 30-year Plan.xls planning/budgeting spreadsheet, the retiree (or experienced financial professional) can make realistic forecasts of these items as they will rise and fall over time.

Be aware that there may be some exceptions such as healthcare costs, which could rise moreso over time.

Also, keep in mind that most expenses inflate to some degree over time. For example, even though your monthly food bill in retirement may be half what it was during your family-raising days, that half-amount will continue to inflate each year.

Don’t Forget These Other Factors

There are a few other factors that may influence your income in retirement: market volatility, and potentially proceeds from an inheritance.

As you consider the future, it’s prudent to heed two other important rules of thumb: (a) don’t make a plan based on financial “hope”; and (b) if something good may come to pass (e.g., an inheritance), keep it in mind but not necessarily as part of your core retirement plan.

Market Fluctuation Effects on Portfolio: Depending on how your portfolio is allocated, the value of your assets may go up and down, contingent on however the markets they are in perform. No one has a crystal ball, but you need to understand what the impact may be, up or down.

Let’s say you retire at age 70 with a balance of $500,000 in a “qualified” account, or an account with pre-tax dollars. Then you started taking withdrawals at 70.5 due to required minimum distributions.

Here are two potential scenarios:

- Assume average annual account appreciation of 3%

- At 89 years old, you would be withdrawing an annual RMD of: $27,402

- With an account balance of: $311,286

- Assume average annual account appreciation of 6%

- At 89 years old, you would be withdrawing an annual RMD of: $48,650

- With an account balance of: $570,178

If you look at scenario two, you would end up with a higher balance than what you started out with. But there is no guarantee that this would happen.

After all, you would be withdrawing and spending down not average returns, but compounding portfolio returns. There is also the possibility of sequence risk which can have a stronger effect on income in the early years of retirement.

The takeaway from this illustration is to show that some careful planning can go a long way in a retirement income strategy.

Inheritance: Generally, people have some idea what kind of inheritance they may get from their loved ones. But what is usually unpredictable is when that inheritance might be distributed, and how much.

If you take the conservative approach, you won’t build your retirement plan around a guesstimate of what that inheritance might be and spend that money in advance.

It’s better to leave out this hope as a core component of your plan, instead building a comfortable plan with what you have accumulated on your own.

In this case, patience is a virtue.

Some Closing Thoughts

Make sure you have open and honest and regular conversations with your spouse about what level of income you want to achieve in your retirement.

Also, consider consulting with a financial professional from SafeMoney.com, who can help you facilitate this discussion and make informed decisions. If you are ready for personal guidance, financial professionals at SafeMoney stand ready to assist you.

Use our “Find a Financial Professional” section to connect with someone directly. Should you need a personal referral, call us at 877.476.9723.