When you are still working, a rock-solid financial plan will do wonders for helping you accumulate money for retirement. This strategy will laser-focus on growth and accumulation as top goals. With a financial advisor’s help, you could stay on track with your plan and gradually build your savings for later years.

But things change as you near retirement. This period is called the ‘retirement red zone‘ for a reason. It’s a time when new planning is needed. Your financial plan will need to change gears, in some ways, in its focus from growth to retirement income.

This can be tricky in some cases, as today we face different challenges in retirement than those before us did. Longer living is one such issue now.

It’s a very real concern for many retirees, as one study by Allianz Life found. In the study, six in 10 retirees ranked running out of money while they are still living as a greater fear than death itself.

Just like the plan for growing your money during your career, an income plan can help you maximize your lifetime cash-flow. In turn, you can better enjoy the hard-earned fruits of your lifetime of work.

Many years of hard work brought you to this point. Now it’s time for your money to work and let you enjoy a comfortable, lasting lifestyle. Read More

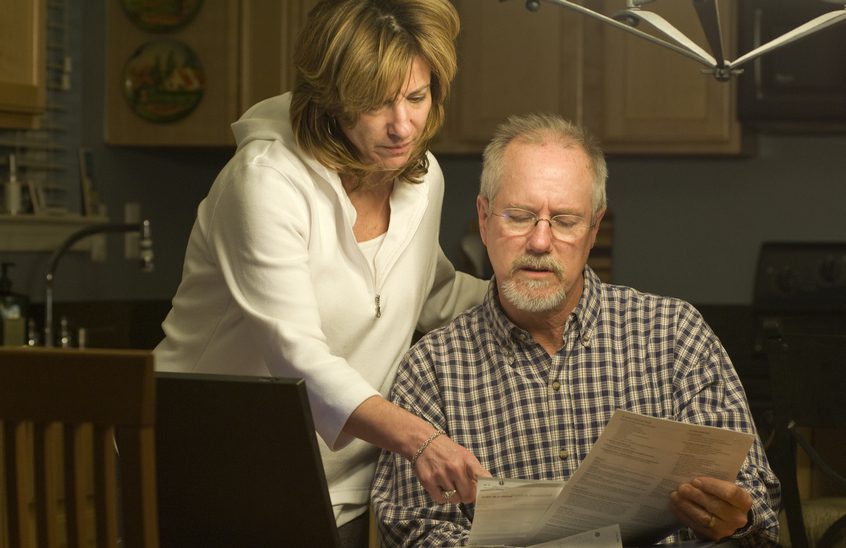

Earlier in your career, you focused on saving and growing your money so you could pursue your financial goals later in life. You might have worked with a financial advisor to do this.

Over the years, you socked away money in a retirement account and maybe even grew an overall portfolio. That meant having and following a strategy with a focus on accumulation and asset allocation. But as we reach the so-called retirement red zone — that crucial period of a decade before and into retirement — new planning is essential.

The income you earned from your career likely won’t be the same once you retire. Then there is the challenge of making your money work for you.

How do you ensure that the income you draw from your portfolio is as efficient and tax-wise as possible? You want to be sure that your money lasts as long as you need it to in retirement! Read More

Franklin Templeton’s annual Retirement Income Strategies and Expectations Survey (RISE Survey) for 2020 has been released. This is the ninth year the RISE Survey has been published, offering valuable insights from Franklin Templeton’s RISE Study.

The survey examines the concerns and attitudes of retirement savers, providing interesting data for both planners and savers. It features insights from various generations on their readiness for retirement and their strategies for achieving financial goals before stopping work.

As usual, this year’s RISE Survey offers valuable insights from Franklin Templeton’s RISE Study. Here’s a roundup of some findings that might be helpful for your own retirement planning efforts.

As another year passes by, more people join the ranks of retirees. Since 2011, roughly 10,000 baby boomers have turned 65 years old each day, according to Pew Research. It predicts that trend to go on until 2029.

From second-act careers to volunteering and entrepreneurship, baby boomers are already reshaping the mold of retirement. And they are bound to keep redefining it, as record-breaking millions are set to leave the workforce.

With a new era of retirement living on the horizon, it’s prudent to take note of our retirement income planning strategies.

Will they provide reliable income streams and financial security for what could well be a decades-long retirement? Do they give a long-term assurance of you being able to enjoy your desired lifestyle? Or when it comes to these goals, does your income strategy have more of a question mark hanging over it?

In their career years, many people work with a financial advisor to build their life savings and plan to continue so in retirement. One notable survey of 200 advisors by investment company Incapital shows how advisors are preparing today’s retirees for the economic uncertainties of tomorrow.

The survey’s focus? What retirement assets these financial advisors were using to generateretirementincome for their clients. Read More

Calculating how much income you will need for retirement isn’t necessarily an easy task. Your health expenses will probably increase, but your mortgage payments may decrease or stop. Meanwhile, other expenses might continue to change over time.

Of course, you likely won’t have to deal with payroll taxes as much. Chances are you will also see expenses tied to employment, from transportation to a professional wardrobe, decline as well. But other costs may appear in retirement, from pursuing long-sought hobbies to traveling or spending more time with loved ones.

Although you may not even know where to start when trying to estimate how much retirement money you will need, there are a few rules of thumb that you can follow to help get you started. Read More

Nobel prize winner William Sharpe calls it the “nastiest, hardest problem in finance.” What is that? Decumulation, or the process of building a dependable lifelong income stream from your retirement savings.

It’s no wonder millions of Americans are asking if they will have enough money to retire comfortably. Between rising health costs, multiplying risks, and the real possibility of “lifelong” referring to what can be a very long time, there are multiple priorities to juggle as you build a personal retirement strategy.

Many Americans worry about whether their life savings and income will last for the rest of their lives, as a recent survey found.

In the poll of 3,119 adults, aged 25-74, the majority of retired individuals (71%) felt confident that their savings and income would last. Meanwhile, just 42% of working-age Americans said they had that confidence.

The survey findings were published by the Alliance for Lifetime Income, a non-profit funded by life insurance carriers and asset managers to educate the public on annuities. Read More

Today, Americans bear more financial responsibility for their retirement than ever.

The days of receiving monthly pension checks are gradually fading. According to Willis Towers Watson, only 16% of Fortune 500 companies were offering pensions to new hires in 2017, down from 59% of firms in 1998.

Defined-contribution plans like 401(k) accounts are taking their place. And this shift is huge. Now, people must count on them, IRA assets, and personal savings to create income streams that might need to last for a very long time.

How long? Potentially decades. The Society of Actuaries estimates that among married couples who are 65, there is a 72% chance that one spouse will live to 85. Not just that, one of them has a 45% chance of reaching age 90.

In other words, someone may spend as much as one-third of their life in retirement. In the face of that, how do you ensure your nest egg lasts for the rest of your lifetime?

While the answer is different for everyone, a new study offers some fresh insights. The Georgetown University Center for Retirement Initiatives partnered with Willis Towers Watson to explore different ways to generate income in defined-contribution retirement plans.

Their findings show how various lifetime income options, whether as a combination or as stand-alones, can help retirees better enjoy lifelong financial confidence. Read More

With more Americans turning 65 every day, one of the most pressing questions in financial planning is: How to make your money last in retirement? Today’s retirees are redefining aging, diving into second-act careers, entrepreneurship, volunteering, and travel. However, longer lifespans also bring challenges, such as creating a dependable monthly income stream that lasts. While there isn’t a one-size-fits-all answer, new research offers insights. Experts from the Stanford Center on Longevity and the Society of Actuaries tested nearly 300 strategies to help retirees generate income safely and efficiently, especially for middle-income households.

Editor’s Note: This article presents some simple ways to strengthen your income confidence in retirement. As you read about how you can make your money last in retirement with different income strategy options at your disposal, check out this debate by two economists on the security of the $3 trillion Social Security trust fund. It’s just another personal reminder of how our personal financial security is ultimately up to each of us.

Determining how much money you need in retirement is both a mathematical and a personal issue. Like a fingerprint, the answer is unique to you and your spouse.

That is why it’s so important to discuss your 30-year retirement plan early – or in other words, definitely some time before you actually retire. And just not early, but often. This approach will help ensure you and your spouse are on the same page.

Here are a few guidelines you can use in your determination of how much money you need in retirement for a comfortable lifestyle. Read More

If only retirement income planning were as easy as answering one question: “What is your number for lifetime retirement security?”

That would be nice if retirement boiled down to just one number. But this oversimplifies what it takes to enjoy a secure retirement because, in truth, it requires a customized income planning approach.

Why? Because determining how much money you need in retirement is just as much a personal question as it is a mathematical one.

Just think about your goals and what you might need financially to make them happen. Do you plan to travel? To begin a career ‘second act’ by getting involved with entrepreneurship or consulting? To donate time and resources to causes that are near and dear to you personally?

Bottom-line, everyone will have different income needs. So, here are five important tips to help guide you through your retirement income planning process. You can also further explore some topics by checking out the other SafeMoney articles linked to throughout this piece. Read More

Start a Conversation About Your Retirement What-Ifs

Start a Conversation About Your Retirement What-Ifs

Already working with someone or thinking about getting help? Ask us about what is on your mind. Learn More

What Independent Guidance Does for You

What Independent Guidance

Does for You

See how the crucial differences between independent and captive financial professionals add up. Learn More

Stories from Others Just Like You

Stories from Others

Just Like You

Hear from others who had financial challenges, were looking for answers, and how we helped them find solutions. Learn More

Sign Up for Our Newsletter

Get a monthly email on the latest news, tips, and practical strategies involving your retirement and money.

Among many other topics, learn how you can make your money last for as long as you need it, can protect your wealth against current and evolving risks, can maximize your income, and can stay retired comfortably.