More Americans Losing Sleep Over Money than Before Great Recession

Note: This is the fourth part of a month-long series on financial awareness in the U.S., and how investors are planning – or not preparing – for retirement. Here are some important takeaways that are keeping Americans from financial security and peace of mind.

For the first time in a long while, Americans are feeling more stressed than ever. If surveys are any indicator, money concerns are a big part of it. In fact, more Americans are losing sleep over money issues than before the Great Recession.

According to CreditCards.com, 65% of Americans report having insomnia over money issues – a 9-point jump from 56% in 2007. And what accounts for these new, high levels of stress? Here’s a quick look at the sleep killers for Americans in 2017.

Top Financial Stressors

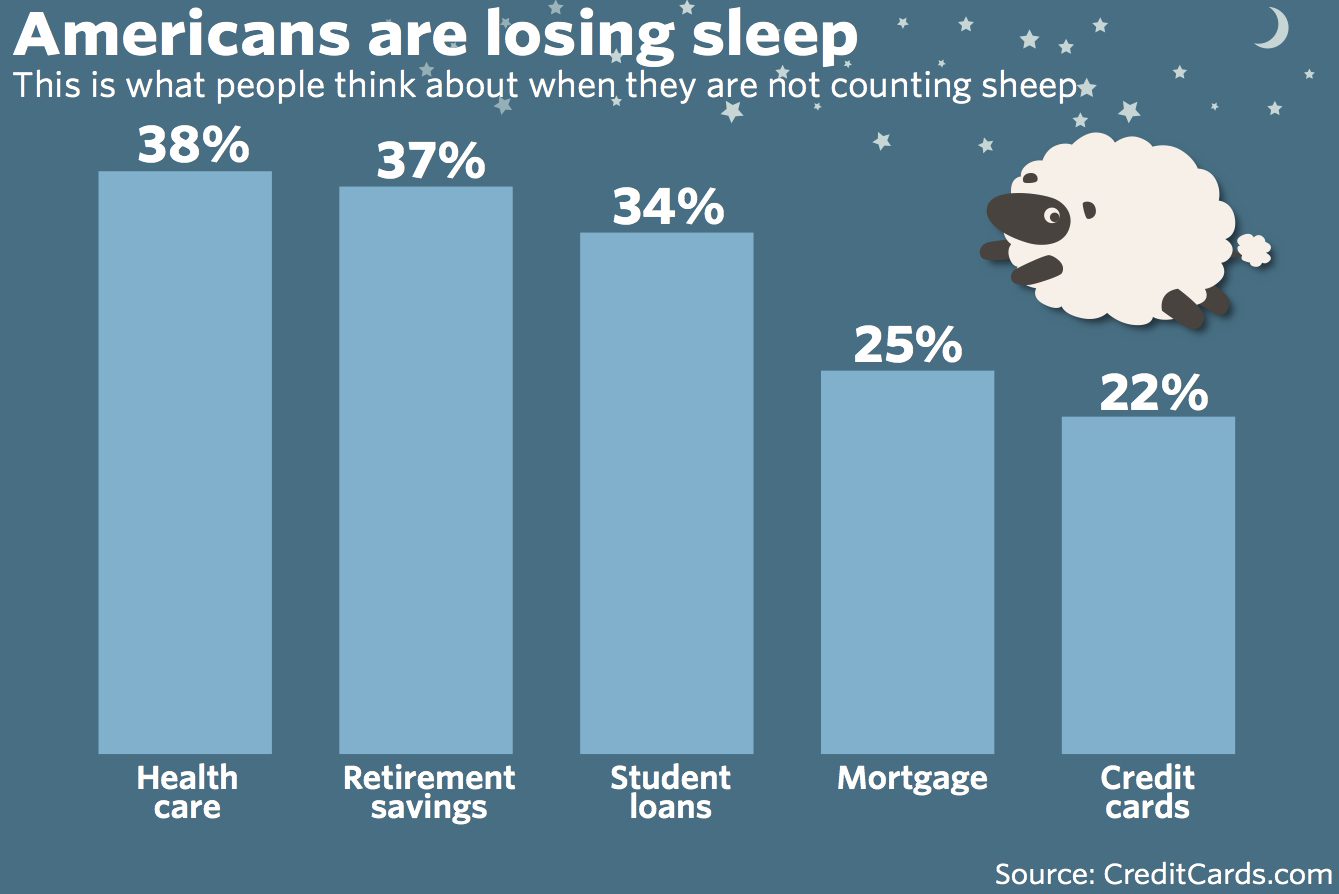

CreditCards.com reports the following as the top factors keeping Americans up at night:

- 38% of Americans worry about healthcare or insurance bills, the top concern

- 37% fret over saving enough for retirement

- 34% lose sleep over anxiety about educational expenses

- 26% don’t sleep due to worrying about mortgage or rent bills

- 22% are concerned about credit card debt

Source: MarketWatch.com, “America’s insomnia problem is worse than before the Great Recession,” Kari Paul, CreditCards.com.

These findings mirror findings from other surveys. In February 2017, a study by Merrill Lynch and Age Wave on retirement savings found similar concerns. In that survey, Americans expressed as their top three financial concerns in retirement:

- Costly health issue affecting themselves or a loved one (49%)

- The impact of inflation on day-to-day living (46%)

- Not having enough money to do they would like (44%)

Other concerns including outliving life savings, having to live on a fixed income, rising taxes, not being able to find work if needed, and earning low yields from the stock market. And with other financial stressors on the rise, it’s no wonder Americans are feeling the heat. For instance, U.S. credit card debt topped the $1 trillion mark in February 2017, according to Federal Reserve consumer data.

Financial Illiteracy, a Crippling Factor for American Wellbeing

Jim Chilton, CEO and Founder of the Society for Financial Awareness, says much of the blame can be laid on financial illiteracy. In this case, illiteracy doesn’t mean that someone is ignorant or dumb, but rather has not been in a position of learning about effective financial management. This lack of financial education leads to people making bad money decisions – which open wide the floodgates for stress, anxiety, and more financial headaches.

In a recent article on April, National Financial Literacy Month, for the Union-Tribune, Chilton says this perpetual pattern of bad money decisions-stress-financial headaches is observable in retirement planning. Instead of a carefully laid out plan for reaching the retirement finish line, many of us think of retirement as a happy accident.

“Often when we hear ‘So and so is retiring’… we do two things…,” Chilton writes. “First – we think that individual is so lucky to be able to quit work and go pursue his/her desires. Second – we reflect on our situation and often become quickly disenchanted, belaboring the fact we don’t have enough money to finish, what happens if we have a calamitous medical issue, what if, what if, what if????”

But retirement shouldn’t be reduced to a milestone that someone is fortunate to reach. Rather, it’s achievable with careful consideration of future needs, goals, and circumstances over a long period – planning which accounts for “living another 25, 30, 40 years from now.” Indeed, with systematic planning and preparation, retirement can indeed be a meaningful life chapter.

“As all of us age, our self-worth and relevance is always ‘in play.’ Some folks retreat, fade away, and then pass away. Others live life to the fullest. They’re engaged in activities, travel, grand- parenting, hobbies, and volunteer work,” Chilton comments on the importance of post-work life quality in the Union-Tribune. “Being active is a necessity. The transition from ‘your career to your rear’ is an important slipping point in your self-significance as you move into retirement.”

“With proper planning and an enthusiastic attitude for life, your retirement years can bring great joy and build self-purpose. It’s definitely a new chapter when you leave the last job.”

Start Putting the Best Foot Forward Today

As a non-profit public benefit organization, SOFA believes that financial wellness starts with education. They offer no-cost, comprehensive financial literacy workshops for organizations of all types, from small businesses and community groups to institutions of worship, corporations, and governmental agencies. To see the financial education opportunity SOFA can bring to your community, visit http://sofausa.org/.

If you are ready to see if your retirement finances on the right track, we can assist you. Use our Find a Licensed Advisor section to connect directly with an independent financial professional, and to request a personal strategy session to discuss your needs and goals. And should you have any questions or concerns, call 877.476.9723.