Social Security 101 — How Much You Know About Your Benefits Matters

Guess what, class. The results are in… and most of us did not pass a very important test. Nearly half of Americans age 50+ failed a basic Social Security quiz, according to a newly released nationwide consumer poll by MassMutual Life Insurance Company.

Why should this news alarm us all? Because Social Security is a major income source for many Americans in retirement. And if we don’t know how to maximize our benefits, or even know what questions to ask regarding how to get our best payout, it can hurt us. We may be leaving money on the table when we need that income the most — whether enjoying healthy income for your lifestyle or enjoying greater income certainty for monthly retirement expenses.

In some sense, it’s as if each point not scored is potentially a dollar amount of benefits we may lose, unless we start paying closer attention. It’s time to consider how much in Social Security benefits we have accrued and start exploring strategies to maximize them.

“Getting Social Security right is critically important to inform plans for other income stream needs later in life as it may be difficult, and sometimes not even possible, to hit the reset button,” said Mike Fanning, head of MassMutual, U.S. “This is not a retirement planning conversation. This is a longevity planning conversation, and near-retirees have the power and responsibility to ensure that they protect and receive every dollar they deserve in Social Security retirement benefits when the time comes.”

Social Security 101

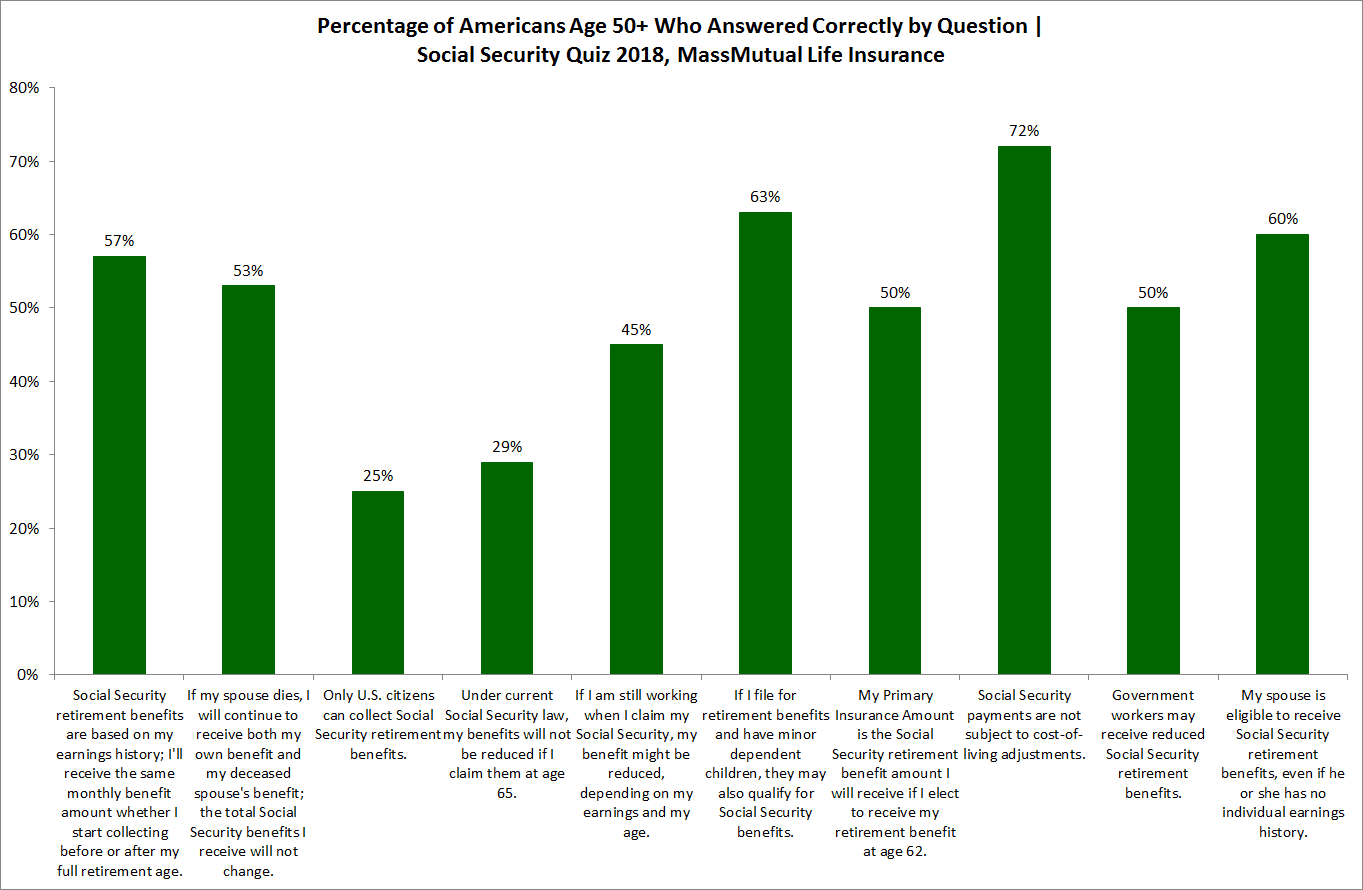

Even though 47% of the near-retirees failed this recent MassMutual Social Security quiz, that number is better than the 62% of people age 50+ who failed a similar quiz by MassMutual in 2015. Overall, the quiz consisted of these questions:

- Social Security retirement benefits are based on my earnings history; I’ll receive the same monthly benefit amount whether I start collecting before or after my full retirement age. (True or False.)

- If my spouse dies, I will continue to receive both my own benefit and my deceased spouse’s benefit; the total Social Security benefits I receive will not change. (True or False.)

- Only U.S. citizens can collect Social Security retirement benefits. (True or False.)

- Under current Social Security law, my benefits will not be reduced if I claim them at age 65. (True or False.)

- If I am still working when I claim my Social Security, my benefit might be reduced, depending on my earnings and my age. (True or False.)

- If I file for retirement benefits and have minor dependent children, they may also qualify for Social Security benefits. (True or False.)

- My Primary Insurance Amount is the Social Security retirement benefit amount I will receive if I elect to receive my retirement benefit at age 62. (True or False.)

- Social Security payments are not subject to cost-of-living adjustments. (True or False.)

- Government workers may receive reduced Social Security retirement benefits. (True or False.)

- My spouse is eligible to receive Social Security retirement benefits, even if he or she has no individual earnings history. (True or False.)

The amount of people who answered correctly, per each question, is shown in this graph. You can try the quiz yourself at the MassMutual site here.

Before we start patting ourselves on the back, here’s an even more unsettling statistic: Only 14% of this survey’s respondents who were age 50-59 have created an account on the Social Security Administration’s web site to view their earnings history and check their account for accuracy. Yes, that means 86% of people surveyed in that age range reported they have never even checked in on their Social Security account.

Before we go any further, if you are in the same account-less situation as the 86%, take a moment to establish your account so you can see what Social Security has recorded as your earning history and what it believes your benefit will be. You can do this by visiting: https://www.ssa.gov/myaccount/.

If there are mistakes in your earning years, say that you find one year is blank when you actually earned income that year. The sooner you point out mistakes and request corrections, the more likely you are to get them fixed, according to the Social Security Administration.

What You Could Be Missing

If you calculate the present value of a household’s monthly Social Security benefits, it could total more than $1 million, says David Freitag, a Social Security expert with MassMutual. People really need to know how it works, he says, adding: “Knowledge is power when it comes to Social Security and retirement.”

From the SocialSecurity.gov website come statistics that prove why lifetime benefit amounts are so important:

- The typical 65-year-old today will live to age 83

- One in four 65-year-olds will live to age 90; and

- One in ten 65-year-olds will live to age 95

“You may need your income to be sufficient for a long time, because people are living longer than ever before, and generally, women tend to live longer than men,” according to Thinking of Retiring?, a consumer guide that can be downloaded from the site.

Do You Know Your FRA from Your PIA?

Back to that poor showing respondents made in that MassMutual survey, about half of Americans age 50 and older don’t know that their benefit will be reduced if they claim their Social Security benefits at age 65.

This surprised the researchers since the full retirement age, or FRA, has been moving up for more than 15 years. If you born in 1937 or earlier, your FRA—the age at which you would receive 100% of your primary insurance amount (PIA)—was 65.

Born between 1938 and 1959? Your FRA ranges from 65 and two months to 66 and 10 months. Born 1960 or later? Your FRA isn’t until age 67.

“In other words, unless you were born in 1937 or earlier, your Social Security benefit will be reduced from the full PIA if you claim before age 65,” the surveyors point out. If you were born in 1938 or later, this chart will tell you how much your benefit will be reduced if you claim before age 65 as well as before your FRA. “It’s important for people to know their full retirement age,” says Freitag.

That chart shows that if you were born in 1960 or later and claim benefits at age 62 instead of your FRA of age 67, you can expect a 30% reduction in your benefits—not just until you reach age 67, but for the rest of your life.

Now that We Have Your Attention…

Any Social Security decisions should always be based on the claimant’s personal circumstances, especially age, work status, personal earnings history, individual health status, personal lifespan expectations, and so on.

And couples have even more at stake. The most serious reduction in benefits a spouse could suffer if planning should go awry? A substantial 35% loss in benefits. That’s why it’s important to work with an experienced, Social Security benefits-knowledgeable financial professional who can help coordinate benefit-taking choices between spouses. Most are likely to have different work histories, earnings records, and even periods of years worked.

Nobody wants to leave money on the table when that benefit can go to the person who worked their whole life to earn it. Don’t let that person be you. Consult with your trusted financial professional to improve your Social Security IQ and bolster your retirement nest egg.

Need Help with Creating an Income-Secure Retirement Strategy?

For many households, Social Security benefits are a foundation of a retirement income strategy. But they are just one of many moving parts. Overall, the goal of a sound retirement income strategy is to generate reliable income streams that last as long as you need them in retirement.

If you could benefit from the personal guidance of a financial professional, assistance may be a click away. Financial professionals are ready to help you at SafeMoney.com. Use our “Find a Financial Professional” section to connect with someone directly. Should you need a personal referral, call us at 877.476.9723.