As 2019 begins, two new surveys suggest that both advisors and economists aren’t so optimistic about where the economy is headed.

This kind of insight from industry experts is useful, but especially to those who are approaching retirement. Knowing what pundits and advisors believe could lie ahead, and exploring what action can be taken in case of any untimely disruptions to their portfolios, is critical to those within five to 10 years of retirement.

So, what do advisors and economists see when they look ahead? They see the shakiness of 2018 leading to a potentially rocky 2019. Read More

A new year has dawned, and you can feel the anticipation in the air. People everywhere have scribbled down their New Year’s resolutions, as 2019 has swept in the allure of new beginnings.

A world of opportunity awaits!

Perhaps with a nod to another passing year, many of us will put eating healthier at the top of our list of resolutions. Hitting the gym more often (or even at all), being more productive with our time, and perfecting our work-life balance are perennial New Year’s Resolution favorites.

And for those in their 50s who have visions of their ideal retirement, the New Year is an ideal opportunity to take stock of what they want to achieve. It’s a time to evaluate where they are in terms of reaching that goal, and to reflect on whether they need to create or refine a retirement plan that will help them get there.

Especially for those who are planning on retiring within the next five years, here are three New Year’s Retirement Readiness Resolutions. Read More

With age comes wisdom – and apparently the ability to better handle unexpected expenses, according to the Society of Actuaries (SOA).

In their recent study, the SOA analyzed financial risk management across generations. Chief among their findings? That “the ability to handle unforeseen expenses increases with age, peaking with Early Boomers and then declining for the Silent Generation.”

The SOA based its finding on the fact that 6 in 10 Early Boomers say they could afford a $10,000 expense using their savings or emergency funds. Yet “only 46% of Millennials would use their savings, which is not surprising since they have lower assets and more competing financial priorities.”

Those in the Silent Generation remain vulnerable. The SOA reports that half of them aren’t able to use their savings for an unexpected $10,000 expense. Read More

Whether you are considering purchasing an annuity or you already have one, there are some key mistakes to avoid in order to benefit from annuity ownership.

The pitfalls below have tripped up many annuity buyers. Our insider tips on knowing what to look out for can prevent you from experiencing the same fate. Use these tips to help you in simplifying your annuity buying decisions or in optimizing your annuity contract as part of your retirement strategy. Read More

Buckle up, everyone. The holidays are just around the corner. And while they bring a spirit of joy and cheer, they can also be a stressful time for many Americans.

From Thanksgiving dinners and holiday shopping to seasonal parties and family get-togethers, there is no shortage of events in which folks participate.

Aside from the festivity, fellowship, and merriment, however, people can “feel the heat” in their money matters in a number of ways. And how might that be?

The pressure to overspend, for one. According to a recent survey by NerdWallet, a little over half of all Americans (51%) say they “typically overspend” on gifts.

Meanwhile, 39.4 million Americans are still paying off debt from last year’s holiday spending spree. And gift shopping is just one of many seasonal expenses that can keep the holiday cash register ringing.

Expenditures such as these can put the strain on retirees, who are more likely to have fixed incomes than other age groups. Not only that, the pressure of growing debt loads can have an impact on people’s retirement goals, not to mention any other financial objectives they may have.

But there is good news. Taking the right steps can go a long way toward achieving more financial security. If you, and your partner, are in your 50s or 60s, it’s good to start laying out your goals, mapping out a strategy for your future, and taking action so your money can work hard for you.

Here are some steps you can take to improve your financial wellness and potentially be more confident for the years ahead. Read More

That is how a surprising number of retirees feel about their tax planning. In a recent study by Nationwide Retirement Institute, staggering proportions of retired Americans wished they had done more to prepare for their sometimes-surprising tax bills.

The survey was revealing. An estimated 60% of future retirees, 70% of recent retirees, and 75% of those retired for more than 10 years said they are only “somewhat knowledgeable” or “not at all knowledgeable” about tax planning in retirement.

That’s right. Three of every four people retired for at least a decade still admit to feeling less than certain about planning for taxes in retirement. Read More

Good news, Social Security beneficiaries! Every year in mid-October, the Social Security Administration announces any cost-of-living adjustments to benefits – or “COLAs.” On October 12, the agency said that Social Security recipients would see a 2.8% COLA in 2019.

A rise in the cost of energy products, not to mention an increasing cost of shelter, were big inflationary contributors, according to experts. Both of those cost categories have heavy weightings within the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), the Department of Labor index on which COLAs are based.

For Social Security beneficiaries, the increased benefit payouts will start in January 2019. People receiving SSI benefits will see the increase on December 31, 2018. Read More

If you have contributed for a long time to a 401(k) plan, chances are you have built up considerable assets. You are to be commended for this effort. It takes discipline and focus to accumulate wealth over time.

Having reached this point, you may now want to explore options outside of your plan. If you are past your late 50s, you might have an opportunity with an in-service withdrawal. Many people with 401(k) accounts assume that their funds are locked tight until they retire.

What they don’t know is that they might be able to access their funds while still working at their employer. This mechanism is formally called an in-service withdrawal.

But what exactly is an 401(k) in-service withdrawal, under what conditions can you take one, and what consequences are there for doing so? Read More

For skiing enthusiasts, the concept of ups-and-downs is quite exhilarating. Just the thought of cutting powder on tall, sloping moguls can make even the “hard cores” blush.

But as recent market volatility reminds us, the goodwill doesn’t apply to ups-and-downs in every situation. Sometimes it can bring just the opposite.

Earlier this month on Morningstar, Director of Personal Finance Christine Benz observed how equity market down-spurts can disrupt a retirement portfolio.

Portfolio losses might not matter as much as when people are younger, as they have time to recover – and to grow past the point when portfolio asset values dipped. In fact, Benz writes, for those with many years to retirement (or under age 50), “not taking full advantage of the historical outperformance of riskier asset classes is a bigger risk than being too conservative.”

But as retirement draws near, some flight to safety may well be a prudent course of action. Benz explains: “At that life stage, you’re much more vulnerable to what retirement planners call sequence of return risk. That means that if you encounter a calamitous equity market early on in retirement and need to spend from the declining equity portfolio, that much less of your investments will be left to recover when stocks finally do.”

And what if a portfolio has gone into reverse mode? “Your only choice to mitigate sequence of return risk–assuming your stock portfolio is in the dumps and you don’t have enough safe investments to spend from–will be to dramatically ratchet down your spending,” Benz says. “Needless to say, that’s not something most young retirees are in the mood to do.” Read More

Photo Credit: Associated Press. All rights reserved, source link.

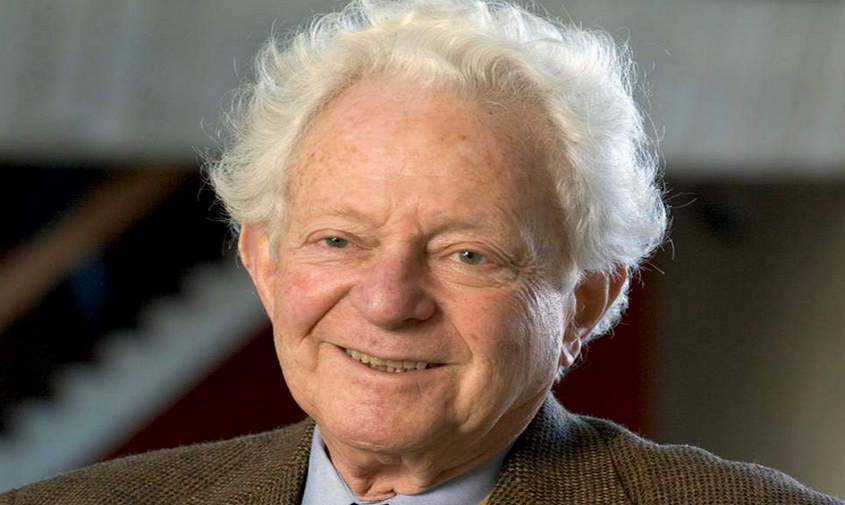

Nobel laureates are certainly top achievers. In 1988, Leon Lederman won a Nobel Prize for his work in physics. Apart from award-winning research into subatomic particles, he is famous for coining the infamous name of the Higgs bosin: the “God particle.”

Lederman passed away in a nursing home in Idaho on October 4. He was 96, according to the Associated Press. The AP describes him as a “giant in his field who also had a passion for sharing science.”

While Lederman’s contributions to science speak volumes, another striking story of him emerges from a past headline by NBC News.

And what happened? In 2015, the physicist was forced to auction his Nobel medal so he and his family could cover healthcare expenses. The medal sold for $765,000. It was a winning bid of $633,335 plus a buyer’s premium that drove the medal to its $765k sell price.

It’s yet another example of how high-cost retiree healthcare needs can change the financial situation of any of us. Read More

Start a Conversation About Your Retirement What-Ifs

Start a Conversation About Your Retirement What-Ifs

Already working with someone or thinking about getting help? Ask us about what is on your mind. Learn More

What Independent Guidance Does for You

What Independent Guidance

Does for You

See how the crucial differences between independent and captive financial professionals add up. Learn More

Stories from Others Just Like You

Stories from Others

Just Like You

Hear from others who had financial challenges, were looking for answers, and how we helped them find solutions. Learn More

Sign Up for Our Newsletter

Get a monthly email on the latest news, tips, and practical strategies involving your retirement and money.

Among many other topics, learn how you can make your money last for as long as you need it, can protect your wealth against current and evolving risks, can maximize your income, and can stay retired comfortably.